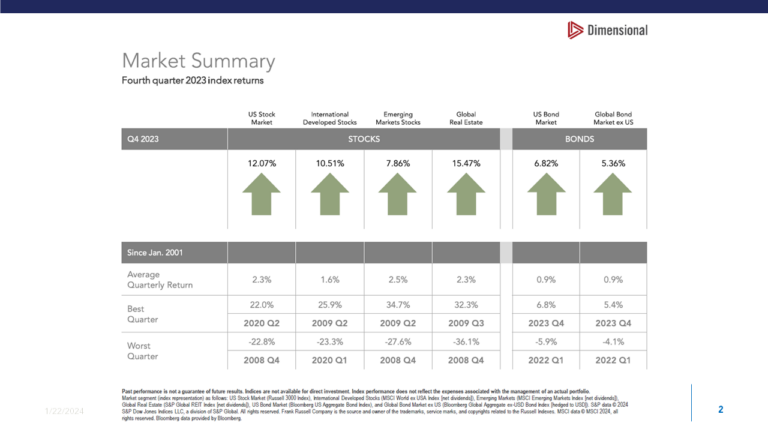

Level’s Steven Elwell, CFP®, discusses first quarter market performance in this video. Extra emphasis added regarding the upcoming Presidential election

This website uses cookies for web analytics and marketing purposes. You can block saving cookies to your hard drive at any time, by changing the settings of your web browser. By continuing to use this website without disabling cookies in your web browswer you agree to saving cookies to your hard drive. Learn more in our Privacy Policy.I AcceptPrivacy Policy