Be sure to watch our continuing video blog on this topic here: https://youtu.be/RXdZf2TAwRs

“The business of life is the acquisition of memories. In the end that’s all there is.” Carson, the butler from Downton Abbey

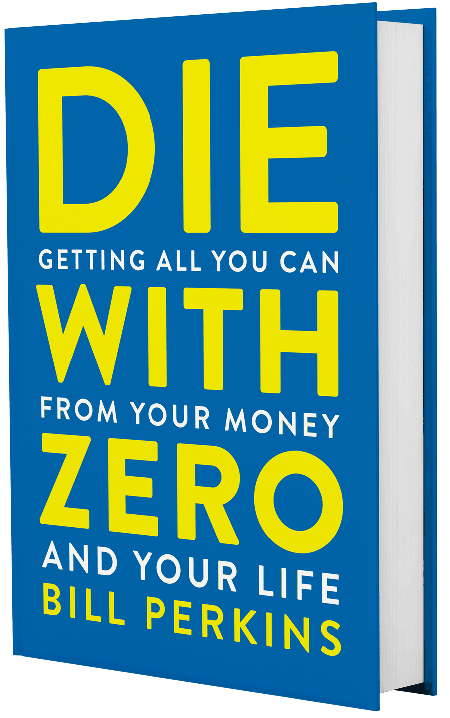

The above quote is central to the book: “Die with Zero: Getting All You Can from Your Money and Your Life” by Bill Perkins

I have included ideas from this book in our Retirement Renaissance series because I think these ideas may help retirees live their best possible retirement.

The author, Bill Perkins, is a former energy trader and professional poker player. Note: he is not a financial planner, which brings a different perspective to how one should manage their finances. His focus is on maximizing experiences and life enjoyment rather than maximizing wealth.

Three of the key concepts in the book:

-

- Spending on experiences brings more happiness than buying things*. In fact, memories keep paying off in what he calls memory dividends. The experience can be re-lived as often as one likes. Think about a great vacation, concert or ball game and how many times you have relived those memories yourself or in the stories you tell. On your death bed it will be memories of good experiences, and not possessions, that bring comfort and joy of a life well lived.

- Start experiences early to build memory dividends and be aware of how you time your experiences, because health will affect the ability to have certain experiences. If you love to ski, it is better to plan those trips sooner rather than waiting.

- Dying with zero – the idea that when we die with money in the bank, we have worked, and sacrificed time in our youth to save for the future and it gets left unspent. It is this idea has made me think about how I live my life and how I advise my clients. And which I will continue to expand on in this blog post.

There is no question, we have to save for emergencies and for a time we want or need to walk away from our careers. But, there is a balance between working, building, wealth and living life that can be better managed – can be optimized.

We have been conditioned to focus on the goal of not running out of money, rather than a goal of: how can I get the most out of my money. Not running out of money is important, but this has created a fear of spending in many retirees. I have clients that have many times the amount they will need in retirement and they still will not increase their spending.

When one dies with money remaining in their savings, the work, stress, and sacrifices to build that savings were for nothing. Perkins says that “if you die with savings then you were working for nothing.” One should ask: If I die with too much unspent savings, how many hours of work, time missed being with children, and personal stress does this unspent “nest egg” represent?

Realistically, we know that dying with zero is an impossible goal. The important thing is that it changes the way you think about retirement and your savings. One should ask: how many hours of work, missed events with children, and personal stress does this “nest egg” represent? This may change the frame of reference from one of preservation of wealth to enjoyment of the wealth.

Some of the things that I am starting to incorporate into my financial planning for clients to help them deal with the fear and help them change their thinking are the following:

-

- First and foremost, a narrative change from: “I am here to make sure you don’t run out of money” to: “I am here to help you optimize your retirement life”

- Educating clients that experiences are more valuable than possessions.

- Building more spending into a retirement plan during the first 10 to 20 years of retirement. We know that spending declines dramatically as we age, so we can balance some of the earlier spending increase with lower spending later in life.

- Discussing the benefits of healthy living. As stated in a previous blog, if you don’t have your health you can’t optimize your wealth.

- In some cases, when a client has enough, I advise them to give to children and/or charity now so they can see the money spent while they are alive. Or, pay to have family and/or friends meet at a destination and have that experience.

- Advise on strategies to alleviate some fears clients have of needing money saved just in case they need skilled nursing care or live beyond expectations. This can be done through trusts, insurance, reverse mortgage, or even a longevity account (saving a fixed amount today that will not be used in the plan).

- Be more interactive with clients and the retirement planning software I use. This software is MoneyGuidePro and it calculates a retirement plan success by analyzing 1000 future scenarios and calculating a probability of not running out of money. By working closely with clients and adjusting the spending plan on an annual basis I can explain the tool and help them feel comfortable if we have to pivot due to market or personal circumstances. I also change the narrative from “you have a 75% chance of success” to: “you have a 25% chance we may have to make changes.” This makes clients more comfortable with the projections.

Finally, this book does a great job of effectively getting people to think about money and its purpose. To do more when you are young, to question the sacrifices – this life is about the journey not exclusively the destination of retirement, to question what you spend money on; I liked how he would calculate how many of hours of work went into a purchase, he would ask himself “is that shirt worth 3 hours of work?” And, most profound for me, to help make sure that the years of sacrifice embedded in savings is not lost.

As a financial planner, I don’t necessarily like the title, but the message is powerful.

*This concept is well documented in the book “Your Money or Your Life” 9 Steps in Transforming Your Relationship with Money and Achieving Financial Independence”